South Africa’s Reserve Bank (SARB) has a fintech unit that investigates emerging trends and tests how viable they are. This same unit was the brains behind project Khoka (an interbank payment platform based on Ethereum) last year.

That same unit is now investigating the possibility of transitioning to a digital currency backed by the Rand. SARB recently put out a tender for ‘prospective solution providers in anticipation of a feasibility project on a digital currency’.

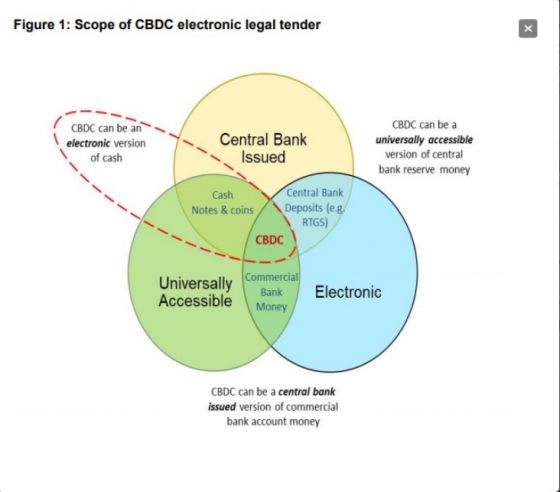

Some of the established targets that the Central Bank Digital Currency (CBDC) for it to be considered viable include:

- The Central Bank Digital Currency (CBDC) will be issued as legal tender by the SARB only;

- CBDC must be complementary to cash and is not intended to replace cash;

- CBDC must be unique in its design and its SARB ownership must be clear and evident;

- CBDC must be issued at one-to-one parity with the rand;

- CBDC must be ubiquitous and accepted as a means of payment by all sizes of business and by the government;

- It must not introduce the risk of destabilising the financial sector and mechanisms must be incorporated to give effect to policy decisions regarding its supply and movement;

- Consumers must be able to own and transact in CBDC without the need for a bank account;

- Consumers and businesses must be provided with the channels to obtain or return CBDC in exchange for cash and commercial bank money;

- It must enable immediate person-to-person transfer of value without clearing and settlement in today’s terms;

- CBDC must be traceable;

- CBDC must be auditable in terms of proof of issuance and ownership.

The fact that the Reserve Bank wants the digital currency to be accessible without need for a bank account is particularly interesting as it brings to question what will happen to the banks if it is indeed adopted.

SARB probably wants to go down this route for the sake of financial inclusion as the banking system tends to leave a large number of citizens unable to access financial services. The Reserve Bank probably also noticed the impact of mobile money on financial inclusion in neighbouring countries, Zimbabwe and Kenya.

It will be interesting to see where this fintech initiative ends up and hopefully SARB shares their findings for all to see even if the project is not a success.