Africa is an interesting continent in many regards. Telecommunications is definitely one of those areas that are interesting. For years, Africa has been heralded as being on the cusp of greatness and the role of mobile network operators hasn’t been downplayed in that narrative.

With this in mind and a general fascination with the telecoms industry we decided to look at the mobile network operators of Africa to see who are the biggest players in this space and which markets are the most significant.

We compiled lists of the largest markets (based on subscriber count), the biggest mobile network providers based on revenues, subscriber count and presence, and the mobile networks with the biggest brands.

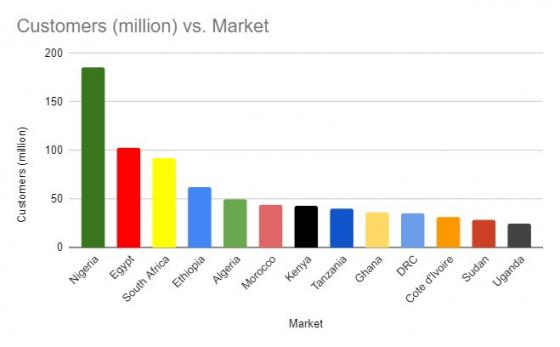

Largest Markets in Africa

From the outset it’s pretty clear that North Africa has a very well developed telecommunications industry. Of the top 10 biggest mobile markets in Africa, there are 3 North African countries. North Africa, on the whole, has 7 countries so this is just under 50% of that region represented here. South Africa is the only country from Southern Africa. The rest of the top 10 markets have countries from East Africa (3), West Africa (2) and Central Africa (1).

PS: It’s important to note that most of the entries on this list are naturally as a result of the fact that most of these are the most populous countries

| Market | Number of customers (million) |

|---|---|

| Nigeria | 185.9 |

| Egypt | 103 |

| South Africa | 91.9 |

| Ethiopia | 62.6 |

| Morocco | 43.9 |

| Kenya | 42.8 |

| Tanzania | 40 |

| Ghana | 36.8 |

| DRC | 35.3 |

| Cote d’Ivoire | 31.7 |

| Sudan | 28.6 |

| Uganda | 24.6 |

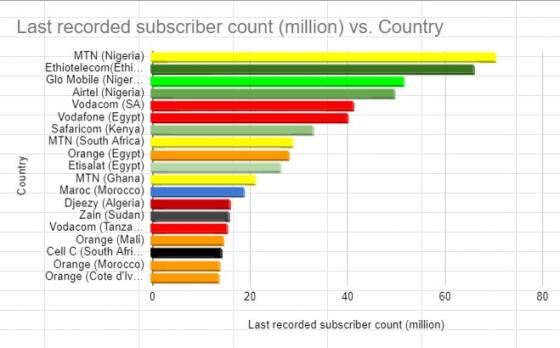

Largest African Mobile Network Operator by subscriber count

The correlation between large populations and large mobile network providers is clear. Nigeria and Ethiopia are the two largest countries in Africa by population. It’s no surprise therefore that MTN (Nigeria) and state-owned Ethiotelecom have the largest subscriber bases.

| Mobile Network Operator | Country | Last recorded subscriber count (million) |

|---|---|---|

| MTN | Nigeria | 70.6 |

| Ethiotelecom | Ethiopia | 66.2 |

| Glo Mobile | Nigeria | 51.7 |

| Airtel | Nigeria | 49.9 |

| Vodacom | South Africa | 41.3 |

| Vodafone | Egypt | 40.2 |

| Safaricom | Kenya | 33.1 |

| MTN | South Africa | 28.9 |

| Orange | Egypt | 28.2 |

| Etisalat | Egypt | 26.4 |

| MTN | Ghana | 21.3 |

| Maroc | Morocco | 19 |

| Djeezy | Algeria | 16 |

| Zain | Sudan | 15.9 |

| Vodacom | Tanzania | 15.5 |

| Orange | Mali | 14.8 |

| Cell C | South Africa | 14.4 |

| Orange | Morocco | 13.9 |

| Orange | Cote d’Ivoire | 13.8 |

When you consider that Ethiopia has a significant portion of their population (over 40%) that are yet to register for telecommunications services – there is remarkable room for growth and continued dominance.

Ethiotelecom’s standing in future reports will be minimised since the Ethiopian government has announced that it will be splitting the mobile network into two and privatising.

Currently, Ethio Telecom has a monopoly over the country’s telecoms

Ovum Africa Digital Outlook 2020

market, and previously Ethiopia has rejected the idea of competition or privatization in the country’s telecoms sector. With a population of about 108 million and a mobile penetration of less than 39% in June 2019, the Ethiopian market holds growth prospects that are likely to be of interest to most major operators on the continent

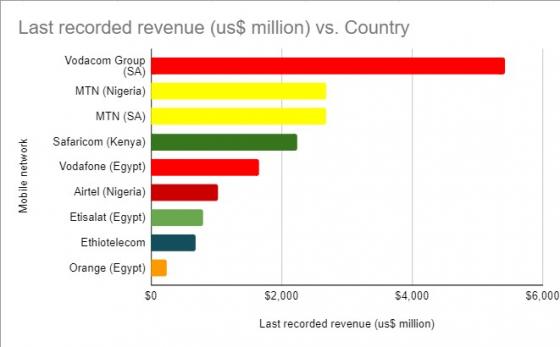

Largest Network Operator by revenue

| Mobile Network Operator | Country | Revenue (US$ million) |

|---|---|---|

| Vodacom | South Africa | $5 416 |

| MTN | Nigeria | $2 687 |

| MTN | South Africa | $2 680 |

| Safaricom | Kenya | $2244 |

| Vodafone | Egypt | $1658 |

| Airtel | Nigeria | $1032 |

| Etisalat | Egypt | $795 |

| Ethiotelecom | Ethiopia | $680 |

| Orange | Egypt | $230 |

Assuming that having the most subscribers would automatically translate to the highest revenues is a fair assumption. Unfortunately, that’s not how it plays out in actuality;

South Africa is better represented in terms of revenue, and Egypt comes a close second with Nigeria and Kenya following. Whilst the subscriber count helps Nigeria, the Average Revenue Per User (ARPU) figures are higher in SA and Egypt. This suggests consumers in these markets have more disposable income to spend on telecoms services

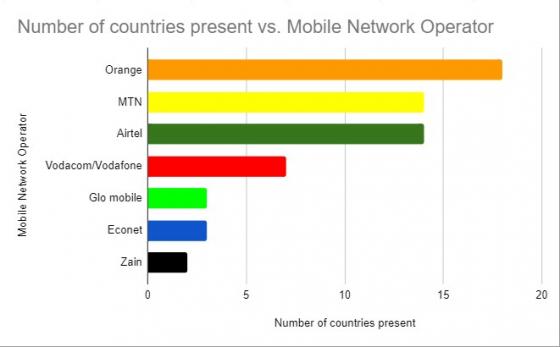

Which operators are in most markets?

There are a number of operators who are in multiple markets on the African continent. Why? Well, the capital expenditure necessary to start a telecoms business is enormous and thus it’s easier for established players to move into new markets than it is for a new player to come up;

| Mobile Network Operator | Number of markets |

|---|---|

| Orange | 18 |

| MTN | 14 |

| Airtel | 14 |

| Vodacom/Vodafone | 7 |

| Econet | 3 |

| Glo Mobile | 3 |

| Zain | 2 |

The most valuable brands?

Every year, Brand Finance complies a report with 150 of the biggest telecoms brands globally. How many African brands made it on the list for 2020? Just 4;

| Mobile Network Operator | Country | Position in Africa | Position globally |

|---|---|---|---|

| MTN | South Africa | 1 | 43 |

| Vodacom | South Africa | 2 | 66 |

| Safaricom | Kenya | 3 | 93 |

| Glo Mobile | Nigeria | 4 | 118 |

MTN’s brand is valued at US$3.3 billion and Brand Finance believes they are well positioned to handle the transition from 4G to 5G;

In recognition of MTN’s increasingly strong leadership position in telecommunication services throughout Africa and the other countries within which it operates, and because of their increasingly resilient network investments, MTN’s brand strength rating has been upgraded from AAA- to AAA.

While their existing network infrastructure will be challenged by the upcoming transition from 4G to 5G mobile phone services, this solid brand strength will put them in a strong position to compete in the future

Brand Finance – Telecoms 150 2020

Ownership

The ownership structures of the telecoms companies mentioned in this report are also quite interesting and the aforementioned point that established players move into “emerging economies” is backed by some of the information you’ll find below;

| Mobile network operator | Country | Ownership structure |

|---|---|---|

| Airtel | Nigeria | Bharti Airtel (20.6%) |

| Cell C | SA | Blue Label Telecoms holds 45%, Net1 UEPS Technologies holds 15%, 3C Telecommunications holds 30%, Cell C Management and Staff hold 10% |

| Djeezy | Algeria | Global Telecom Holding (51.7%) |

| Econet | Zimbabwe | Econet Wireless (Private) Limited |

| Ethiotelecom | Ethiopia | Ethiopian Telecommunications Corporation (state-owned) |

| Etisalat | Egypt | Etisalat (76%), Egypt Post (20%), Other Investors (4%) |

| Glo Mobile | Nigeria | Globacom (20.78%) |

| Maroc Telecom | Morocco | Etisalat (49%), state of Morocco (51%) |

| MTN | Ghana | MTN (97.7%) |

| MTN | Nigeria | MTN (41.5%) |

| MTN | SA | MTN Group |

| Orange | Cote d’Ivoire | Orange S.A. (85%), Comafrique (15%) |

| Orange | Egypt | Orange S.A. (99.96%), minority shareholders (0.04%) |

| Orange | Mali | Orange SA (29.65%) |

| Orange | Morocco | Orange S.A. (49%), FinanceCom+CDG (51%) |

| Vodacom | SA | Vodafone (60.5%) |

| Vodacom | Tanzania | Vodacom (82.2%) |

| Vodafone | Egypt | Vodafone Group plc (54.93%), Telecom Egypt (44.94%), Free Float (0.13%) |

| Zain | Sudan | Zain Group |

What’s the biggest takeaway from all of this? Well ,there’s too much data for there to be one but if I had to pick – it’s simply the fact that the “MTN, everywhere you go” ad I remember seeing for the first time in 2003 was not just a slogan after all…

We will look at fixed telecoms networks in a separate feature article.

Comments

3 responses

I think you should have salvaged some information about where our very own Econet stands. Econet now has the largest data carrier services through Liquid Telcom I Africa south of the Sahara. They supply MTN with bandwidth and also have offered to give their 5G spectrum to Vodacom SA.

Population growth is good for the economy. Are there any barriers to entry into that market. What is government role in new entrants

Hey Jemula, which market particularly?