The Zimbabwean government did a number on banks, suspending loans that are responsible for a third of their revenues. We know that banks are trying to engage the authorities to see if they can’t find a better solution to the abuse of loan funds by the public.

Banks are going about it in a civil way, for fear they could put a target on their own backs. We all know they are fuming in the background. If only we could get an honest reaction to the government’s measures.

For a minute we thought one bank had given their candid response to the president’s controversial measures. A paper was circulating on social media, purporting to be BancABC’s official summary and analysis of the president’s economic measures.

The paper was brutally honest and I imagine that’s how most in the banking industry feel about the government’s policies. However, the paper in question was not from BancABC.

BancABC has unequivocally distanced itself from that document.

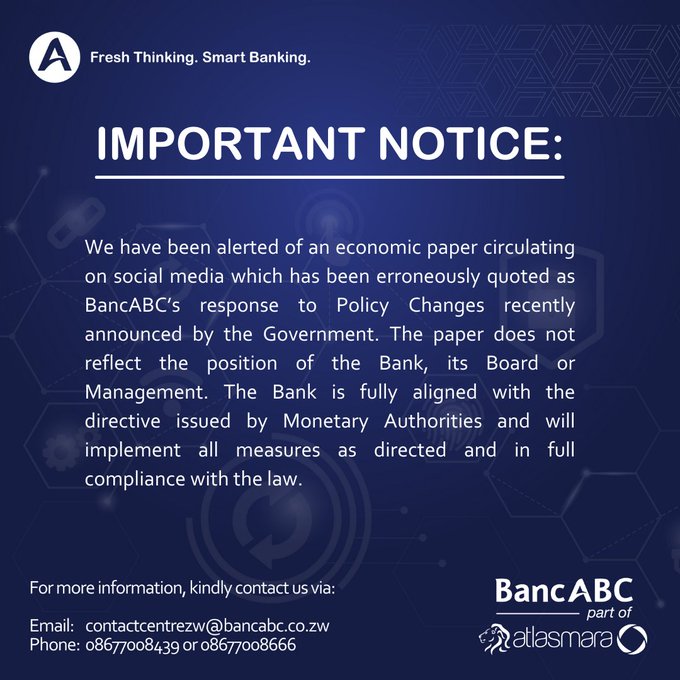

IMPORTANT NOTICE:

We have been alerted of an economic paper circulating on social media which has been erroneously quoted as BancABC’s response to Policy Changes recently announced by the Government. The paper does not reflect the position of the Bank, its Board or Management. The Bank is fully aligned with the directive issued by Monetary Authorities and will implement all measures as directed and in full compliance with the law.

For more information, kindly contact us via:

Email: contactcentrezw@bancabc.co.zw

Phone: 08677008439 or 08677008666

BancABC on twitter

I believe BancABC here. There is no way the paper came from them. Even if they felt that way, they would not put those thoughts on their letterhead. So that rules out this being an accidental leak in my opinion.

Besides, you can clearly see that whoever the author is did not have access to a high resolution copy of the bank’s logo. I could be wrong and this all could have been planned to introduce just doubt if the paper ever leaked. I don’t think that’s the case though.

That said, questions arise. Who wrote the scathing analysis? And even more importantly, why did they try to pin it on BancABC? Why BancABC specifically? Was the choice random or was BancABC firmly in the crosshairs?

Could this be the work of an ex employee or a disgruntled customer trying to get the bank in trouble?

Or chillingly, could this be the work of a rival bank playing dirty? We can’t rule out the possibility.

All that said, you can read for yourself the paper in question. You’ll have to agree the author makes very good points here and betrays a knowledge of the topics in question as well as access to some hard to find data.

SUMMARY & ANALYSIS ON ECONOMIC MEASURES BY PRESIDENT

| Measures | Comments |

| Restoration of lost value on Bank Deposits – Gvt to compensate individuals who had funds below US$1,000 as of end of Jan-19. | – In Feb-19, Gvt abandoned a 1-1 exchange rate peg of the Z$ to the US$, resulting in the exchange rate depreciating from Z$1 per US$ to Z$2.5 per US$. – The Z$ depreciation means depositors lost value of their deposits which at the time were viewed as at par in US$ terms. – At the time of the conversion of the deposits, total deposits which were believed to be at 1-1 to the US$ were Z$8,965m. Comments – This is not the first time Gvt has compensated depositors for loss of value. In 2015, depositors were also compensated following demonetisation of the Z$ during multi-currency period. – These schemes could be a waste of resources as depositors require a stable and predictable economic environment, rather than to be continually compensated for loss of value. |

| Clearance of Foreign Currency Backlog -Gvt undertook to clear Auction allotment backlog by end of May-22. -FX allotment to be settled within 14-days period. -The Auction to allot only available FX | -Lack of political will to implement agreed policy measures is eroding confidence in the economy. -This pronounced exchange rate management framework was agreed a long time ago, and yet Authorities have not adopted it. Comments -The current economic meltdown could have been avoided had the Authorities implemented agreed roadmap on exchange rate management. -As previously highlighted, the current overvalued ZW$ at the auction is creating a fertile ground for arbitrage and generating inflated demand for FX. |

| Continuation of a Multicurrency System -The current Multicurrency currency system will remain in place. -De-dollarisation process will be guided by economic fundamentals. | -The market is not yet ready for the adoption of the mono-currency system as economic fundamentals still fall short of the requisite benchmarks. Comments -Any premature introduction of the mono-currency will lead to further economic instability and market rejection of the local currency. |

| Willing-Buyer-Willing-Seller Foreign Exchange System (WBWS) -The amount that can be traded under this system has been increased from US$1,000 per day to US$5,000 or US$10,000 per week per individual. -Retailers/Wholesalers are allowed to benchmark their pricing to the average WBWS exchange rate. | -So far, the WBWS market has been skewed towards buying FX, which is not ideal. -The WBWS exchange rate is also still low compared to the unofficial market exchange rate, making it difficult to attract significant sellers. |

| Reserve Money Growth -Quarterly Reserve Money growth further reduced from 5% to 0% | -In the past, growth in Statutory reserves despite a 5% RM target growth was a sign that the monetary policy stance was not tight enough as deposits continued to growth. |

| Differential Intermediate Money Transfer Tax (IMTT) -2% to continue to apply to local currency transfers -Domestic foreign currency transfers to attract 4% IMTT | -IMTT has been a contentious Tax since it was first introduced as an attempt to capture the informal sector to contribute to the tax net, as well as harness resources for infrastructure -Since then, IMTT is now used as a broad-based tax for both informal and formal sectors, to assist Gvt in raising its revenue Comments –The high IMTT effectively means that the market will avoid depositing the US$ into the Banking system. -This will increase informalisation of the economy as transactions will be on a cash basis and outside the formal channels. |

| Foreign Currency Cash Withdrawal Levy -Withdrawal of cash above US$1,000 will attract a 2% levy | -These measures are impediment for customers to use the banking channels and this works against financial inclusion efforts. Comments –This is an opportunity for banks to develop digital platforms to support US$ transactions. -The customers will feel discouraged to use the banking system because of the attendant high costs |

| Settlement of FX tax Obligations in Local Currency -Settlement of local currency Tax obligations will be at a WBWS exchange rate | -Following the introduction of WBWS, Gvt should immediately unify the Auction and WBWS exchange rate system. -The existence of multiple exchange rate systems will encourage arbitrage activities and corruption. |

| Liquidation of the Surrender portion of Export Proceeds -Liquidation of surrender portion of export proceeds will be at the WBWS exchange rate | This is commendable as it will improve viability of generators of FX Comments –Major risk relate to the manipulation of the WBWS system, which will result in widening premium. -Ideally, the auction system is no longer serving its purpose as it is a vehicle for arbitrage. -Critically, continuation of Auction entails Gvt paying subsidy (which is the difference between the auction and the WBWS exchange rates) which is not budgeted for. -The existence of a multiple exchange rate system only benefit the elite and is a major source of corruption and arbitrage. |

| Suspension of Third-Party Country Payment on Foreign Payments -Third Party country foreign payments have been suspended | -This is to stem susceptible illicit financial flows |

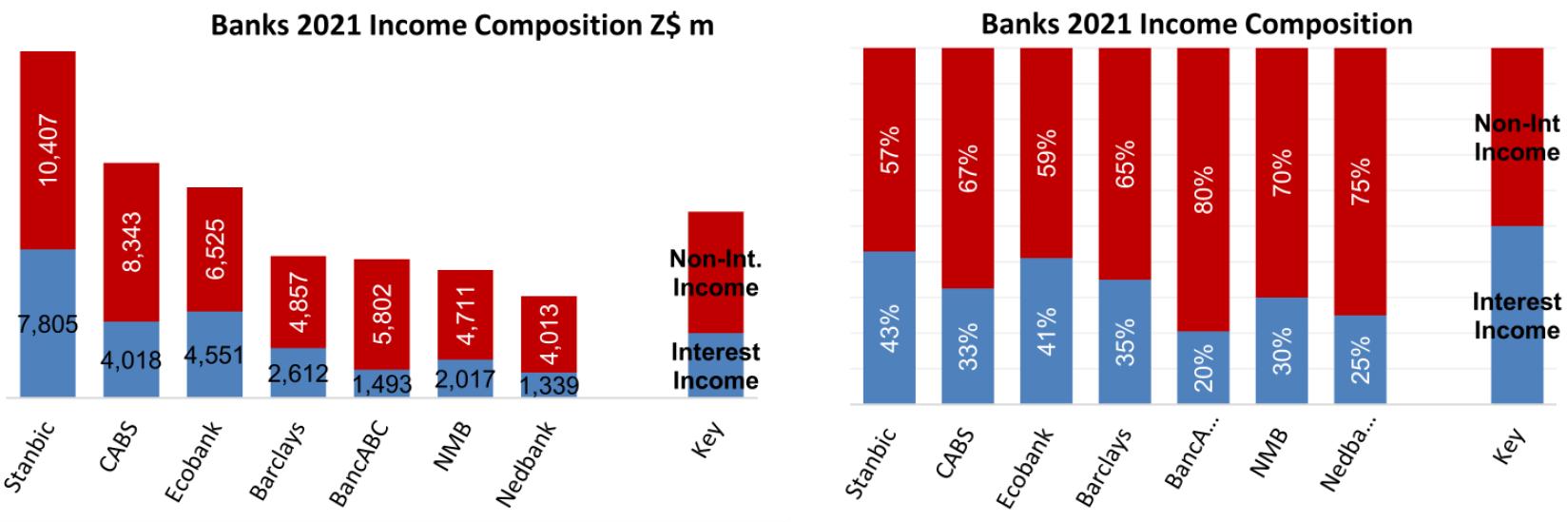

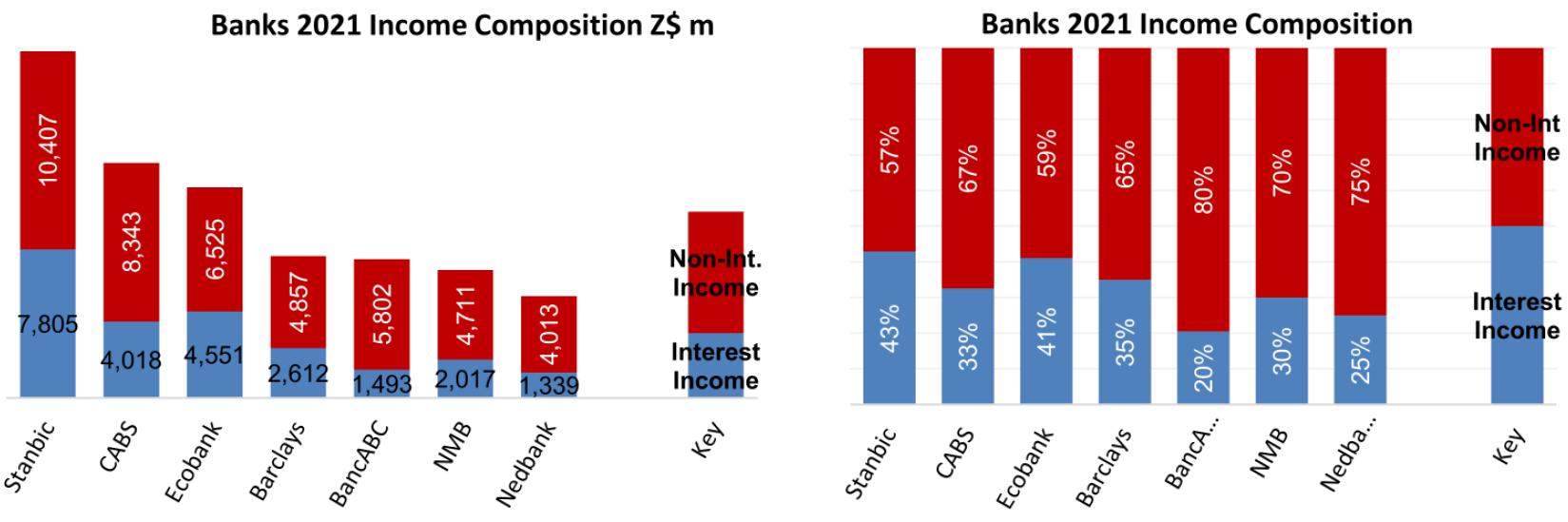

| Suspension of Lending by Banks -Lending by Banks has been suspended | -Growth in Local Currency which in turn is blamed for fuelling parallel market cannot be attributable to bank lending alone, as Gvt is well known for injecting huge liquidity as and when it makes payments to local contractors. -The move to suspend bank lending is unprecedented as it goes against the norm of economic recovery, and contrary to the rational of supporting economic recovery. -Gvt is adopting non-conventional practice in an attempt to avoid dealing with currency reforms. Comments -The Gvt is using a blunt approach to try and address a long-standing issue of currency conundrum. -Bank lending is the core function of Banks financial intermediation process. Banning lending activities will threaten survival of Banks as this will wipe out 20-50% of their incomes. -Consequently, this could push banks to embark on risk and/or non-permissible activities to compensate for the loss of incomes. -This could also push bank charges upwards as Banks devise survival strategies. -On the other side, the companies cannot survive without working capital facilities. This will lead to scaling down of operations, shortages of goods, further price increases, viability challenges and possible company closures and job losses. -No economy can survive without access to working capital. |

| Fostering discipline on the ZSE -Transfer of funds between accounts by brokers is now prohibited -Investment at ZSE for less than 270 days will attract 40% Capital Gains Tax (CGT) | -Markets by their nature are intricately linked and reflect inherent distortions in the economy. -The runaway ZSE performance was a sign of dislocations in the foreign exchange and money markets and the broader economy. -The ZSE is also reflecting the investors behaviour of running for cover in times of economic trouble, as well as lack of confidence in the direction the local currency was taking. -A plethora of regulations impose operational bottlenecks, make the ZSE inefficient and unattractive to foreign and domestic investors. -This has potential to undermine pensioners and new listings. |

Appendix

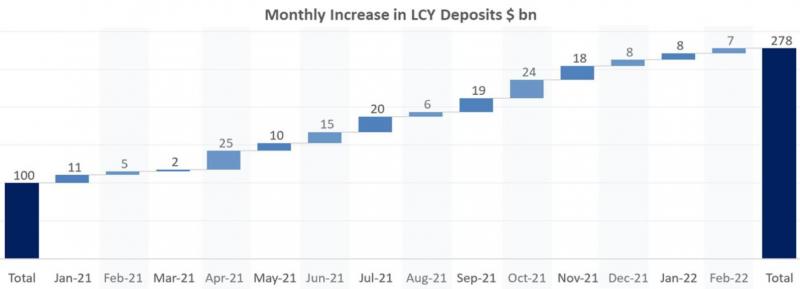

-Gvt believes that the growth in LCY deposits has caused volatility in the FX market.

-While lending by banks has in part contributed to some level of money creation, this only represent a fraction on the drivers of FX volatility

-Growth in LCY deposit is largely blamed on huge Gvt payments in respect of local

contractors & quasi fiscal operations

-Clearly, the huge growth in LCY deposits is concentrated specific months which could be associated with the huge Gvt

payments which in turn triggered exchange rate volatility.

-Banks make 20 50% of their income through interest income, arising from lending activities. Banning lending will therefore endanger their viability.

-Similarly, companies require working capital facilities to restock, increase capacity utilisation and smoothen their cashflows. Prohibiting access to funding will undermine operations, curtail growth, result in shortages of goods and price escalation.

You should also read:

- Suspension of loans: Bank charges are going up, here’s why

- With lending suspended, banks will be okay but microfinance institutions likely to struggle

- 4% forex tax & withdrawal levy: Forever banishing the idea of banking USD

- RBZ on suspension of bank lending. Partly drawn loans are suspended too. What is the rationale behind these decisions?

Comments

One response

I think we no longer need kindergarten economics at RBZ.We need professional economic minds at that institution.whatever is coming out of that place is a bad omen to the whe of Zimbabwe.The paper is churning out the truth as it is on the ground and this ban on banks to lend,will backfire with serious consequences.If we continue along this path,by December we will be living in 2008 not in 2022.