We inherited the capitalist economies of the West, which cannot function without a decent financial system. Our struggles in Zimbabwe are partly due to not getting this right. A financial system’s core parts are banking, insurance, and capital markets.

- Banking deals with the management of money, credit, and other financial activities.

- Capital markets enable the buying and selling of stocks, bonds, etc., allowing businesses to raise money and investors to grow wealth

- Insurance protects individuals and businesses from financial losses due to unexpected events.

Today, we talk about insurance, which was severely impacted by the country’s currency problems.

We all understand that a currency cannot succeed if there is no trust in the government issuing it. Unfortunately, losing that trust affects the financial system to its core.

It only takes one person getting peanuts on their life insurance plan to set off a crisis. In Zimbabwe, thousands, if not millions, saw their plans turn to dust as the Zimdollar collapsed. Hence, it won’t surprise you that Zimbabweans are under-insured.

We are slowly getting back on the horse, so let us look at the short-term insurance industry to see what’s what.

The Insurance and Pensions Commission (IPEC) released the Q1 report for 2024, and here are some of the highlights.

How the insurers are doing

IPEC reports that there are 20 insurance companies and 10 reinsurance companies (reinsurers offer insurance to the insurers).

7 of the 20 insurers reported negative insurance service results, indicating losses. That’s 35% of the insurers reporting losses. The industry as a whole reported less than US$2m (ZW$43.65b) in profit in the quarter.

It was even worse for the reinsurers. 56% (5 out of 9) of them reported negative insurance service results, indicating losses from offering insurance coverage. Total profits for reinsurers as a whole were just over US$200,000 (ZW$4.45b) in the quarter, so the ones that posted profits did significantly better than those that posted losses.

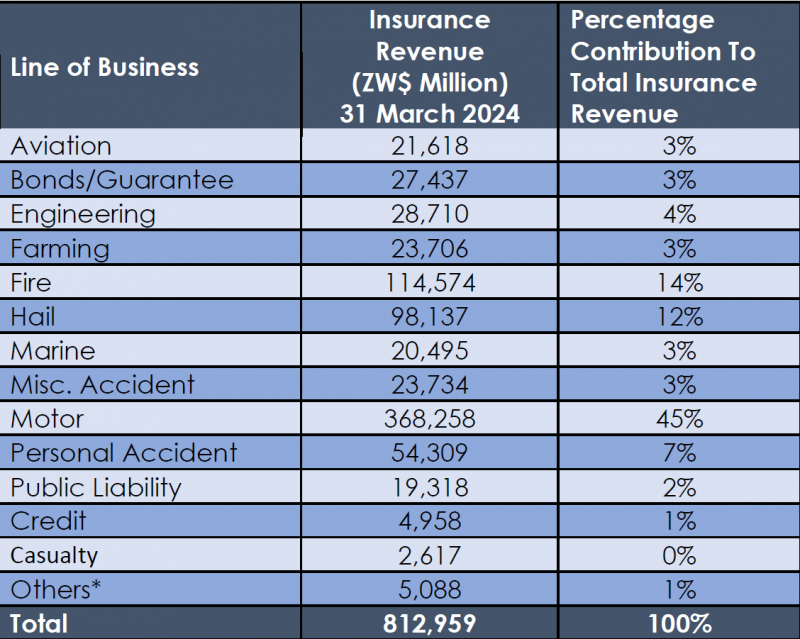

Short term insurers

We acknowledged that Zimbabweans are not currently enthusiastic about insurance, so there are no prizes for guessing which line of business contributes the most to insurers’ bottom lines—motor insurance.

Motorists cannot weasle out of insuring their vehicles, and as more and more ex-Jap cars hit our streets, the insurers have benefitted.

Motor insurance contributes 45% to revenues, while fire and hail come in at 14% and 12%, respectively.

For a country that relies on agricultural output, it is surprising to see farming contribute only 3%. Maybe farmers mostly utilise long-term insurance. One hopes.

When it comes to business in foreign currency, motor was still on top with 40%, but fire saw its contribution rise to 21%, and hail came in at 10%.

What’s concerning for these short-term insurers is that 8 of the 20 companies reported negative working capital ratios. That means they might not have enough money on hand to pay their bills and keep running smoothly in the near future.

So, 8 out of 20 might struggle to maintain daily operations in the near future, which is troubling. This means they might struggle to settle claims, which is a big deal.

However, it’s to be expected in the challenging economic environment we find ourselves in.

Reinsurers

For reinsurers, fire contributed 51% to revenues, while motor came in second with 10%, and miscellaneous accidents were third with 9%.

It was pretty much the same for earnings in foreign currency. Fire contributed 49%, and motor 9%.

Reinsurers are doing a better job of managing their cash on hand (working capital). Only 1 of the 9 reinsurers had a negative working capital position.

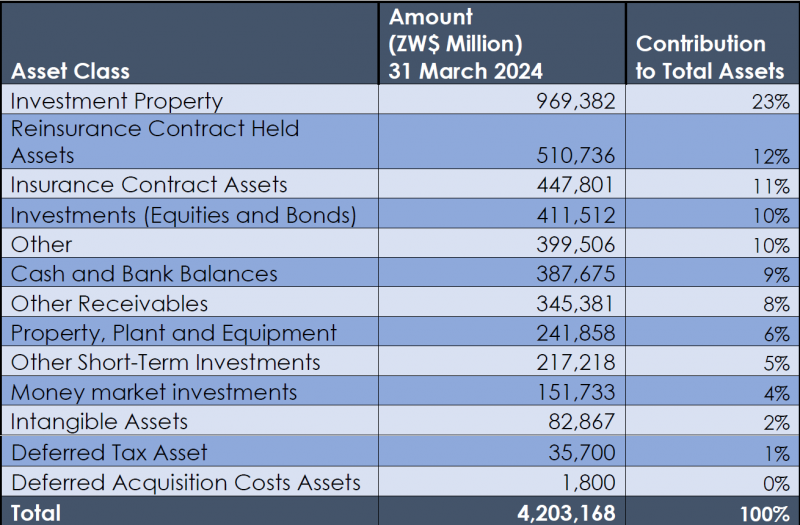

What insurers invest in

It’s always interesting to see what insurance companies invest in. These companies have some of the sharpest financial managers, certified actuarial scientists if you can believe it.

When we pay our premiums to insurance companies, they invest that money, and it hopefully grows such that they can pay out claims as they come and also turn a profit.

So, in a country with various challenges, including unpredictable inflation and high interest rates combined with a small and not very diverse financial market, what do these companies invest in?

Direct insurers had the following assets:

Property

As you can see, 23% of their assets are real estate. They hold this property for two main reasons: to earn rental income and to grow in value (or at least preserve it).

For a long time in Zimbabwe, real estate has been the go-to investment vehicle. So, it’s not surprising to see direct insurers hold about a quarter of their assets in property. Too bad real estate is not easy to access for the vast majority of us.

Interestingly, IPEC’s guidelines say investment property should not exceed 10% of assets, but the insurers more than doubled that. Property cannot easily be turned into cash, which is why the guidelines say it shouldn’t exceed 10%.

This points to there not being better options in the financial markets to invest in.

Prescribed assets

The picture becomes even clearer when we consider that only 7 out of 20 insurers complied with minimum prescribed ratios.

That means there are some investments that are imposed by the government, mainly composed of Treasury Bills, Corporate Bonds, and Equities for the insurers.

The government believes those areas are important for national economic development and social welfare. So, by law, insurers are supposed to hold at least 10% of their assets in those prescribed classes.

As a sector, the insurers held 10% in equities and bonds as the law prescribes, but that figure was mainly carried by the 7 that complied. The other 13 held less than 10% in those assets.

IPEC acknowledges that the low uptake of prescribed assets was due to their exposure to inflation and lack of value preservation.

The other assets

You saw that 12% of assets were reinsurance contract held assets. That simply means the money a direct insurer expects to get back from the reinsurer if it has to pay out claims. Those are the insurers’ own insurance plans.

Then you also saw that 11% were held as insurance contract assets. It’s simply the money an insurance company expects to earn from its customers who have insurance policies. This includes the premiums they’ll pay, minus the amount the company expects to pay out for claims.

We cannot cover everything in the report here. You can dig into it yourself and find more interesting details. I thought the above was a good starting point.

4 comments

appreciate the analysis… there property interesting. they should enforce the 10% because we can’t compete with them. in the end how do you insure in a hyperinflation economy

Netone is no longer available on techzim airtime services😥… Is there any other option besides *788#

paynowtopup

https://www.topup.co.zw/

Paynow, the B2B and B2C payments platform celebrating 8 years. Announces USSD code *828#

https://www.techzim.co.zw/2022/11/paynow-the-b2b-and-b2c-payments-platform-celebrating-8-years-announces-ussd-code-828/

paynowtopup

Paynow, the B2B and B2C payments platform celebrating 8 years. Announces USSD code *828#