While last week was all about the official Mukuru wallet launch, it was also an opportunity to celebrate 20 years of Mukuru.

The company turned 20 last year and for those not familiar with its story, here is the timeline:

Then here is the full rundown of how it all came about:

Twenty years ago, a simple idea was born from two Zimbabwean-born entrepreneurs, Rob Burrell and Brian Nugent, on a hike in the Chimanimani Mountains—an idea that would connect families across borders, breaking barriers that once seemed impossible.

In 2004, Mukuru started as a platform allowing people in London to buy international talk time vouchers, giving Zimbabwean families the gift of connection at a time when calling home wasn’t an option. What began as a solution for communication soon transformed into something far greater: a financial services platform dedicated to making life easier for millions.

Today, Mukuru stands as a leading next-generation financial services platform, serving over 17 million customers across Africa, Asia, and Europe. With more than 250 million transactions to date, we have expanded beyond international money transfers to provide a full range of financial solutions tailored to our customers’ needs. Our operations now span over 70 countries and more than 570 remittance corridors, ensuring that financial inclusion is not just a vision but a reality.

Our Zimbabwe Story: A Journey Rooted in Impact

Zimbabwe holds a special place in our story. It was here that Mukuru’s journey truly took shape, evolving from an idea into a multinational organisation at the forefront of bridging the digital and cash divide.

In 2009, we made it possible for migrant workers to send US dollars from the UK and EU to their families back home. Since then, we have grown into a trusted name, empowering over 3 million Zimbabweans with access to financial services that are safe, reliable, and affordable.

Having been here for the past 20 years, in 2016, Mukuru grew from 5 branches in Zimbabwe. Since then, we have built 250 owned service points—40% of which are in rural areas—alongside 500 partner access points across the country. Our iconic orange booths, branches, and partner locations are more than just collection points; they are symbols of accessibility, security, and convenience, ensuring that even those in the most remote areas can receive their money without stress.

Over the past two decades, our partners have played a critical role in shaping Mukuru into the leading financial services platform it is today. Their contributions have been instrumental in the technology we use, the infrastructure we have built, and the customer-centric approach we pride ourselves on.

A Game-Changing Milestone: The Deposit-Taking Microfinance Institution (DTMFI) Licence

In 2024, Mukuru reached a historic milestone: being awarded a Deposit-Taking Microfinance Institution (DTMFI) licence by the Reserve Bank of Zimbabwe, a that journey started in 2012.

This is more than just a licence—it is a gateway to financial empowerment. It allows us to extend banking-like services to communities that have long been underserved, enabling individuals to save securely and access services that were once out of reach.

With this licence, we can drive the adoption of digital financial solutions, offer small loans to entrepreneurs, help families pay school fees, and provide support during emergencies. More importantly, it strengthens our mission to bridge the gap in financial inclusion, particularly for women, youth, people with disabilities, and those in rural areas.

Transforming Lives Through Financial Inclusion

In Zimbabwe, where 63% of the population resides in rural areas, access to financial services remains a challenge. But Mukuru is changing that. Our extensive network of service points ensures that even those without traditional banking access can send and receive money with ease. Digitisation is a critical part of this transformation—reducing costs, saving time, and making financial services more inclusive.

For many women balancing household responsibilities, individuals with disabilities who face challenges in accessing physical banking points, and small business owners striving to grow, Mukuru is more than just a financial service—it’s a partner in progress. By providing digital solutions, we help eliminate barriers and ensure that financial services are accessible to all, no matter where they are.

Aligning with National Goals for a Better Future

Mukuru’s commitment to financial inclusion aligns closely with Zimbabwe’s National Financial Inclusion Strategy, spearheaded by the Reserve Bank of Zimbabwe. As digital transformation takes centre stage in the country’s economic growth, we stand ready to play our part in driving meaningful change. Our 20-year journey of serving over three million Zimbabweans reflects our shared vision with the regulator—to foster economic empowerment, increase household income, and create opportunities for a better future.

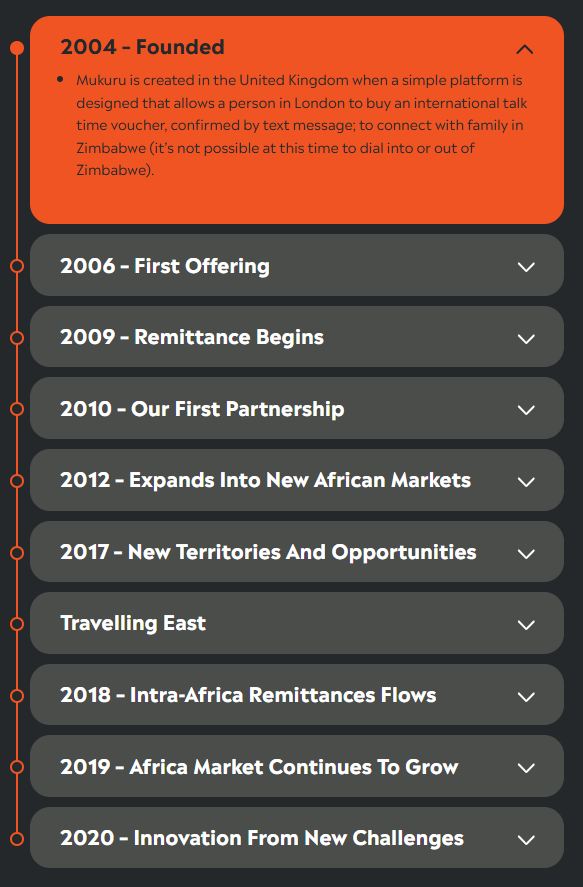

Now, let’s get back to the timeline and expand it out a little:

2004 – Founded

- Mukuru is created in the United Kingdom when a simple platform is designed that allows a person in London to buy an international talk time voucher, confirmed by text message; to connect with family in Zimbabwe (it’s not possible at this time to dial into or out of Zimbabwe).

2006 – First Offering

- Fuel coupons and groceries are added to international talk time. The service is usable only from the UK.

2009 – Remittance Begins

- A platform is developed to enable migrant workers to send USD from the UK and EU to their families in Zimbabwe. Partners are activated in the destination country to make sending and receiving remittances easier, safer and more affordable.

2010 – Our First Partnership

- The Mukuru business in South Africa is formed from a joint venture with Inter-Africa, a Bureau de Change. Most migrant workers are sending home remittances by informal means; this is expensive, unreliable and often dangerous.

- Mukuru grows its technology to enable safer, more reliable electronic remittances and expands its contact centre to communicate with customers in their own languages.

2012 – Expands Into New African Markets

- Technology is developed to aid people in their personal journeys toward financial inclusion. This includes an easily accessible free self-service and army of agents equipped with an Android app to sign-up and serve customers wherever they live.

- Mukuru spearheads a new way to capture KYC (Know your Customer) documents with the support of the South African Reserve Bank. Customers are verified by agents who capture and verify documents like passports and asylum papers at the customer’s place of residence. Instead of being an obstacle, compliance becomes an enabler.

- Mukuru creates a free customer USSD platform and again innovates by splitting a transaction into its various parts. Customers can now create an order, a reference number is texted to them, which they present at a retail partner and pay for their order in cash.

- PEP becomes Mukuru’s first retail partner in South Africa.

2017 – New Territories And Opportunities

- Additional needs and opportunities become apparent with a new customer base that is largely unbanked. The Mukuru Card (backed by Standard Bank) is created to enable customers to have their salaries paid into a money account, shop electronically and pay for remittances.

- Mukuru applies for financial services licences in destination countries and creates its own branch presence, along with customer application agent services and the USSD self-help channel.

Travelling East

- Mukuru brings Asia onboard, working with aggregators in a two year pilot project to ensure efficiency in a new market that demands a richer front-end experience and more sophisticated technological solutions. Mukuru entrenches its presence in India, Pakistan and Bangladesh.

- A Mukuru Orange Booth network is launched during the Zimbabwe cash crisis. The booths enable families back home to receive cash when they need it most. A corresponding app is developed to ensure service to customers remains uninterrupted.

- DRC, Namibia, Ethiopia and Ghana join the Mukuru family.

2018 – Intra-Africa Remittances Flows

- Mukuru activates intra-Africa remittance flows. This significantly increases volume and places its systems under pressure.

- Using a micro-services approach, Mukuru creates its own FinTech solutions to allow for larger volumes and an increasing compliance framework to accommodate regulations in its various countries of operation.

2019 – Africa Market Continues To Grow

- Mukuru onboards Uganda, Eswatini and Tanzania.

- It launches business WhatsApp which soon accounts for 25 percent of its transactions. Mukuru starts work on the upgrade of its app and focuses on its information security capabilities and optimising system performance during peak periods.

- Mukuru carries out three transactions every second and is recognised as a strong FinTech brand with a loyal customer base.

2020 – Innovation From New Challenges

- Mukuru expands into China.

- It purchases several hundred Zoona booths in Malawi which significantly broadens the company’s rural reach.

Mukuru has a global footprint with 60 partnerships that enable more than 100 brands to provide cash out points. Plans include expansion of its Orange Booths and increasing its ability to accommodate the intra-Africa flow of remittances.- The COVID-19 pandemic creates increased uptake of USSD and WhatsApp direct sign-up and demand for electronic products. Mukuru launches Mukuru Groceries and Mukuru Shopping Discounts.

- Mukuru partners with WorldRemit to become a payout partner for WorldRemit remittances across territories where Mukuru has its own booth and branch network.

- Mukuru is listed as one of the leading 150 cross-border businesses globally in the 2020 FXC Intelligence Incumbents vs Challengers in Cross-Border Payments.

Navigating Zimbabwe

As you can see from the above, Mukuru has a big presence outside Zimbabwe, but the country remains important. Many asked both Mukuru Zimbabwe Financial Services Chairman and CEO—Bongai Zamchiya and Doug Tait-Knight, respectively—how it is operating in the challenging economic environment, where many have bemoaned regulatory challenges.

I’ll be honest with you—I don’t place much value in that question or whatever answer you get from it, especially when it’s like the one the two gentlemen gave.

They both said the company has worked well with the RBZ and the government. The Deputy Minister of Finance was invited to the Mukuru wallet launch, as was an RBZ representative, and all parties involved said they work well together.

The reality is that you would not expect Mukuru to say the RBZ and the government are hard to work with in settings like these. It would be unwise to antagonize those parties, and so even if it were the case, Mukuru would publicly tell you it’s been a piece of cake.

So, I ask you to take their responses with a grain of salt. Regardless, the company has only continued to innovate and grow, and so whatever challenges there are, they are dealing with them effectively. That should be the lesson.

Even when many startups will tell you that the regulatory landscape is challenging in Zimbabwe—which it objectively is—there still exists the chance to navigate it. So, I guess that’s the highest praise we can heap on Mukuru.

They have been quietly doing their thing and have not attracted the ire of the Zimbabwean government, which we have seen to be vindictive if it wants—as I’m sure EcoCash would attest.

Anyway, I’m excited to see what the next 20 years of Mukuru bring us. It should be interesting.

Leave a Reply